Mid-Year Financial Review: 5 Steps to Get Back on Track Before December

Use a mid-year financial review to reset spending, rebuild savings, and improve your budget before December.

Feeling Behind Financially? Here’s How to Recover Before December

January is full of financial optimism.

People build savings plans, promise to stop overspending, organize debt payoff strategies, and set ambitious goals for the year ahead.

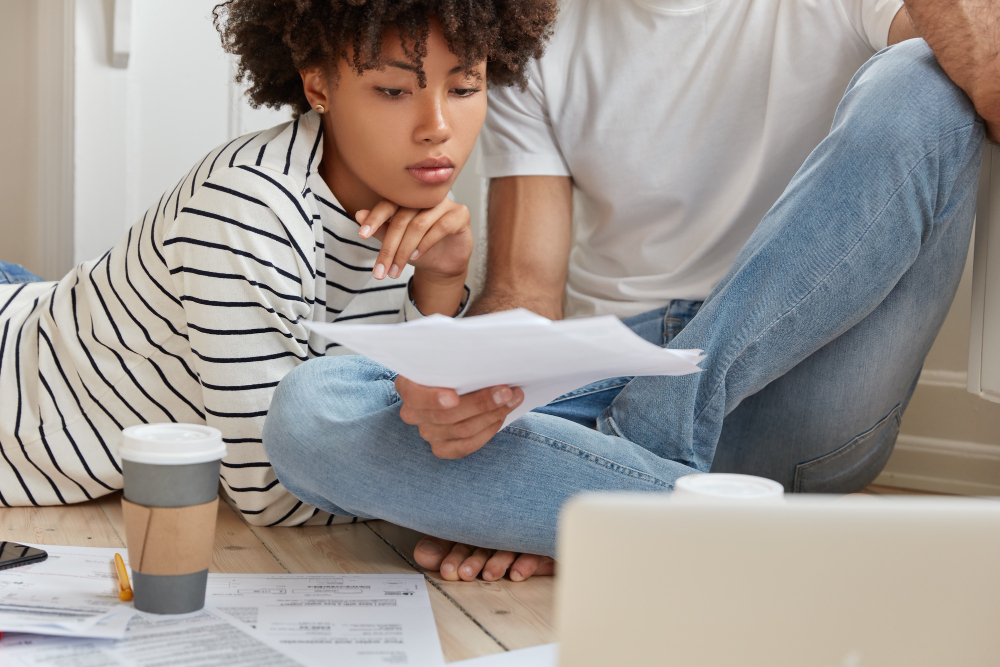

Mid-year financial review strategies to reset your budget, reduce money stress, and finish the year stronger financially. Photo by Magnific.

But once summer arrives, reality usually looks very different.

Inflation keeps pressuring household budgets. Travel season increases spending. Credit card balances rise quietly. Emergency expenses appear out of nowhere.

That is why a mid-year financial review is one of the most underrated financial habits.

Instead of waiting until December to discover you lost control of your budget, a mid-year review gives you time to course-correct while the year is still recoverable.

And honestly, six months is more than enough time to improve your financial position if you approach it strategically.

This guide breaks down five practical steps to help you regain control before the end of the year — without unrealistic budgeting or financial guilt.

Why a Mid-Year Financial Review Actually Works

Most financial mistakes do not happen overnight.

They happen gradually:

- A few extra subscriptions

- More restaurant spending

- Small impulse purchases

- Growing balances on credit cards

- Delayed savings contributions

Individually, these decisions seem harmless.

Together, they slowly reshape your finances.

A mid-year financial review works because it interrupts that drift.

It forces you to stop operating financially on autopilot.

More importantly, it creates a rare opportunity: You still have time to improve the outcome of your year.

Step 1: Analyze Where Your Money Is Really Going

People are usually surprised when they calculate their true monthly spending.

Not because they are irresponsible — but because modern spending is fragmented across:

- Digital wallets

- Credit cards

- Automatic renewals

- Delivery apps

- Streaming platforms

- Buy now, pay later services

A proper mid-year financial review starts with financial visibility.

The objective is simple:

Track your actual behavior instead of relying on assumptions.

Start With These Categories

| Spending Area | What to Review |

|---|---|

| Housing | Rent, mortgage, utilities |

| Food | Groceries, dining, delivery apps |

| Transportation | Fuel, insurance, ride shares |

| Debt Payments | Credit cards, loans |

| Lifestyle | Shopping, entertainment |

| Digital Spending | Subscriptions, apps, memberships |

One useful exercise is comparing projected spending versus actual spending.

Example of Spending Drift

| Category | Planned Monthly Budget | Actual Monthly Average |

|---|---|---|

| Groceries | $450 | $670 |

| Dining Out | $200 | $510 |

| Subscriptions | $40 | $129 |

| Shopping | $150 | $390 |

This is where financial leaks become obvious.

Many households are not collapsing financially because of one huge expense.

They are losing money through consistent overspending in multiple smaller areas.

That distinction matters.

Because small habits are easier to fix than major financial disasters.

Step 2: Adjust Your Financial Goals Instead of Abandoning Them

One major problem with yearly financial planning is rigidity.

People often create goals in January and refuse to adapt them later — even when life changes dramatically.

But financial planning should be dynamic.

Your mid-year financial review should account for:

- Salary increases or reductions

- Inflation

- Family changes

- Medical expenses

- New debt

- Housing costs

- Economic uncertainty

For example:

Imagine your original goal was:

- Save $15,000 this year

By July, you only saved:

- $3,000

Technically, you would now need to save $2,000 monthly to hit the original target.

That may not be sustainable.

Instead of giving up entirely, revise the goal intelligently.

A realistic target creates momentum.

An impossible target creates frustration.

Better Financial Adjustments Often Include:

- Lowering savings goals temporarily

- Extending debt payoff timelines

- Reducing unnecessary fixed costs

- Increasing automated savings gradually

- Pausing nonessential purchases

A mid-year financial review should improve your financial direction — not punish you for imperfect progress.

Step 3: Attack Expensive Debt Before It Gets Worse

Debt becomes dangerous when interest compounds faster than your income grows.

That is especially true with revolving credit card balances.

Recent market data shows many credit card APRs now exceed 20%, making debt repayment significantly harder than it was just a few years ago.

During your mid-year financial review, identify which debts are costing you the most financially.

Debt Priority Breakdown

| Debt Type | Average Interest Range | Financial Risk |

|---|---|---|

| Credit Cards | 20%–29% | Very High |

| Payday Loans | Extremely High | Severe |

| Personal Loans | 8%–36% | Moderate |

| Auto Loans | 5%–12% | Lower |

| Federal Student Loans | 4%–8% | Lower |

High-interest debt quietly destroys financial flexibility.

The more income directed toward interest payments, the less money remains available for:

- Savings

- Investing

- Emergency funds

- Retirement contributions

Smart Mid-Year Debt Strategies

Focus on One Balance First

Eliminating a smaller balance can improve cash flow quickly.

Negotiate Interest Rates

Some lenders may reduce APRs for customers with strong payment history.

Stop Adding New Debt

This sounds obvious, but many people continue using credit cards while trying to pay them off.

Redirect Temporary Income

Tax refunds, bonuses, or freelance income can accelerate debt reduction significantly.

The goal is not perfection.

The goal is reducing financial pressure before year-end.

Step 4: Strengthen Your Emergency Fund

An emergency fund is not just about financial security.

It is about decision-making power.

Without savings, unexpected expenses force people toward:

- Credit cards

- Personal loans

- Payday loans

- Missed bill payments

A mid-year financial review should include a serious evaluation of emergency preparedness.

Basic Emergency Savings Targets

| Savings Goal | Financial Purpose |

|---|---|

| $500 | Small emergencies |

| $1,000 | Short-term financial cushion |

| 1 Month Expenses | Basic stability |

| 3 Months Expenses | Strong protection |

| 6 Months Expenses | Long-term resilience |

Many financial experts recommend saving several months of expenses immediately.

But realistically, smaller milestones create better consistency.

If your emergency fund is currently empty, focus first on building your initial buffer.

That first $500 or $1,000 matters more than most people realize.

It prevents financial emergencies from becoming financial disasters.

Step 5: Prepare for the Most Expensive Part of the Year

One mistake people repeat every year is acting surprised by predictable expenses.

The final quarter of the year is historically expensive because multiple financial pressures happen simultaneously:

- Holidays

- Travel

- Gift shopping

- Seasonal utility increases

- Insurance renewals

- School-related costs

A smart mid-year financial review includes future planning — not just reviewing the past.

Typical Q4 Financial Pressures

| Expense Type | Common Timing |

|---|---|

| Holiday Gifts | November–December |

| Flights & Hotels | Thanksgiving & Christmas |

| Winter Utilities | Late Fall |

| Insurance Bills | End of Year |

| Subscription Renewals | Often Q4 |

Instead of absorbing these expenses suddenly, divide them across the remaining months.

Example

Expected holiday spending:

- $900

Months remaining:

- 6

Monthly savings target:

- $150

That approach dramatically reduces financial stress later.

Preparation is one of the strongest forms of financial control.

Common Mistakes During a Mid-Year Financial Review

Even financially responsible people make avoidable mistakes during financial evaluations.

Ignoring Small Expenses

People focus heavily on major bills while overlooking repetitive spending patterns.

Coffee, food delivery, app renewals, and impulse shopping add up faster than expected.

Setting Extreme Budgets

Aggressive restrictions rarely last.

Sustainable financial habits are usually moderate and repeatable.

Avoiding Financial Data

Some people stop checking balances because they feel anxious.

Unfortunately, financial avoidance usually increases problems instead of solving them.

Comparing Yourself to Others

Social media creates distorted expectations around spending and lifestyle.

Your mid-year financial review should reflect your financial reality — not someone else’s curated image online.

A Simple Mid-Year Financial Review Checklist

Before moving into the second half of the year, review these areas carefully:

Income

- Salary updates

- Side income

- Bonus projections

Spending

- Monthly averages

- Subscription audits

- Lifestyle inflation

Debt

- Interest rates

- Total balances

- Repayment priorities

Savings

- Emergency fund progress

- Retirement contributions

- Automated transfers

Future Expenses

- Travel plans

- Holiday budgets

- Insurance renewals

You do not need a perfect spreadsheet system.

You just need financial awareness.

Final Thoughts

A mid-year financial review is less about fixing mistakes and more about rebuilding intentionality.

Financial progress rarely happens through dramatic overnight transformations.

It usually comes from:

- Better awareness

- Smarter adjustments

- Consistent habits

- Controlled spending

- Realistic planning

And the people who enter December feeling financially stable are often not the people earning the most money.

They are the people who paid attention early enough to change direction while there was still time.

Related content

Life insurance beneficiary mistakes that can cost

Avoid costly life insurance beneficiary mistakes and ensure your policy truly protects your loved ones. Follow these tips.

Keep reading * You will be directed to an external website