Life insurance beneficiary mistakes that can cost your family everything

Avoid costly life insurance beneficiary mistakes and ensure your policy truly protects your loved ones. Follow these tips.

Small errors today can create major problems tomorrow.

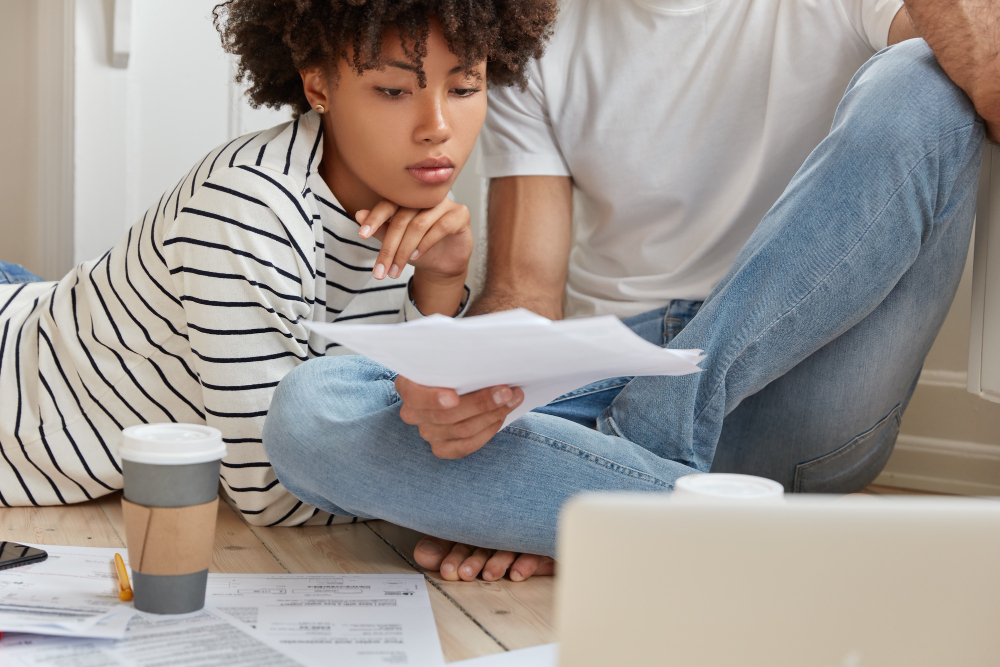

Choosing a life insurance beneficiary seems simple, but small details can create serious consequences later. Many policyholders make decisions quickly and never revisit them, assuming everything will work out as intended.

The reality is different. Outdated information, unclear designations, or legal misunderstandings can delay payments or even send money to the wrong person entirely.

Failing to update beneficiaries after life changes

One of the most common life insurance beneficiary mistakes is failing to update your policy after major life events. Marriage, divorce, or the birth of a child should always trigger a review. When updates are ignored, benefits may go to someone no longer relevant to your life.

This oversight happens more often than people expect. Policies are often set and forgotten, especially when purchased years earlier. As a result, the original beneficiary remains in place even when circumstances change dramatically.

Keeping your policy current ensures your intentions are honored. Regular reviews help avoid confusion and reduce the risk of disputes among surviving family members during an already difficult time.

Naming minors without proper planning

Another frequent issue is naming minors directly as beneficiaries. While it may seem logical to leave money to your children, insurance companies typically cannot release funds directly to minors. This can lead to legal complications and court involvement.

In many cases, a guardian or trustee must be appointed to manage the funds. Without proper planning, this process can delay access to the money and create unnecessary stress. The funds may also be managed in ways you did not intend.

Setting up a trust or naming a legal custodian can prevent these issues. It ensures the money is handled responsibly and used according to your wishes until the child reaches adulthood.

Not adding contingent beneficiaries

A less obvious but equally serious mistake is failing to name contingent beneficiaries. Many people only list a primary beneficiary and assume that is enough. However, if that person passes away before you, the situation becomes complicated.

Without a backup beneficiary, the insurance payout may go through probate. This can delay distribution and expose the funds to legal fees or claims from creditors. It also removes control over who ultimately receives the money.

Adding contingent beneficiaries provides an extra layer of protection. It ensures that even if circumstances change, your policy still serves its intended purpose without unnecessary legal hurdles.

Using unclear or vague beneficiary descriptions

Confusion can also arise when beneficiaries are not clearly identified. Using vague terms like “my children” or “my spouse” without proper legal names can lead to disputes. Ambiguity increases the risk of delays and conflicts.

This is especially problematic in blended families or situations involving multiple marriages. Different interpretations of your wording may lead to disagreements among relatives, sometimes requiring court intervention.

Using full legal names and precise details avoids misunderstandings. Clear documentation ensures that your intentions are followed exactly, minimizing stress for those left behind.

Ignoring alignment with your estate plan

Finally, many people overlook how beneficiary designations interact with their overall estate plan. Life insurance policies typically bypass wills, which can create inconsistencies if not carefully coordinated.

For example, your will may divide assets equally, but your insurance policy might name only one person. This imbalance can cause tension and confusion among heirs, especially if expectations were different.

Reviewing your policy alongside your estate plan ensures everything aligns. Taking the time to coordinate these elements helps create a smoother process and protects your family from unnecessary complications.

Improving financial decision making

A consistent monthly reset sharpens your ability to make better financial choices. With clear data in front of you, decisions become less emotional and more strategic. This reduces regret and increases confidence in how you manage money.

Over time, you rely less on guesswork and more on informed judgment. This shift leads to smarter spending and saving behaviors. Better decisions naturally improve your overall financial health.

Increasing accountability and consistency

The framework creates a sense of personal accountability with your finances. Knowing you will review everything monthly encourages more mindful behavior throughout the month. This awareness helps you stay aligned with your goals.

Consistency is what turns small actions into meaningful results. Even minor improvements, repeated regularly, create lasting impact. This steady approach builds long term financial stability.